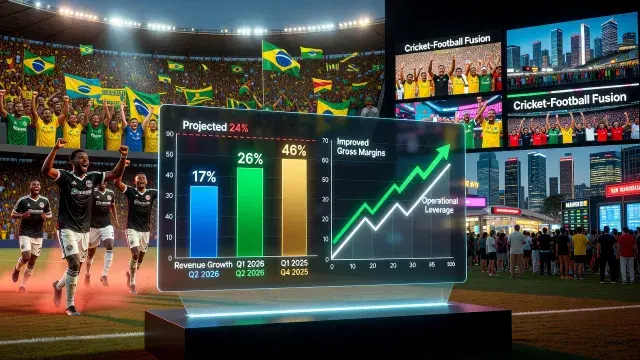

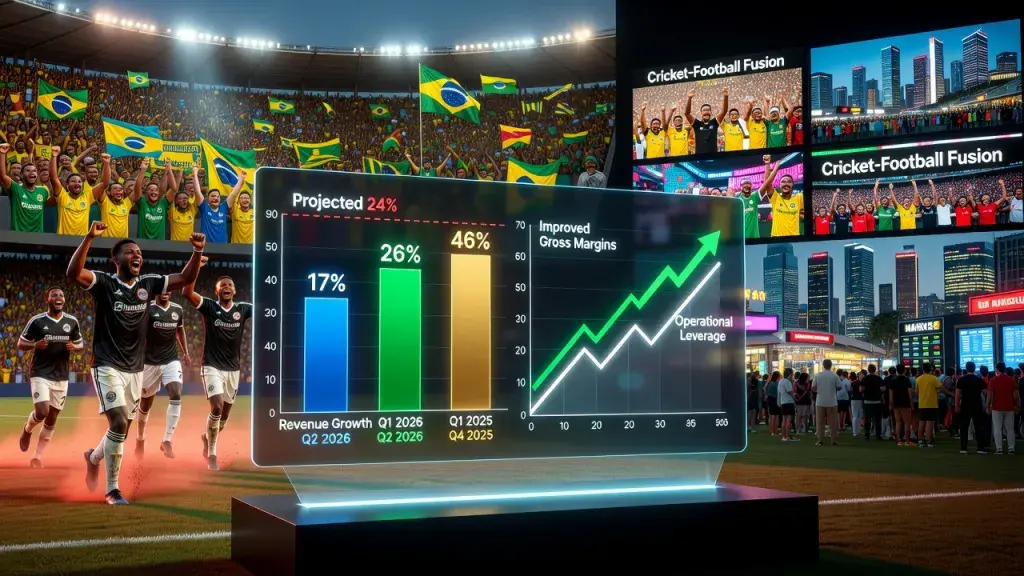

Preliminary sales figures for the second quarter of 2026 show total revenue grew by 17 per cent year-on-year, a meaningful deceleration from the 26 per cent recorded in Q1 2026 and the robust 46 per cent expansion seen in Q4 2025. The result came in below internal projections, which had pointed toward growth of approximately 24 per cent for the period. Despite the softer-than-expected top line, analysts indicate that earnings growth should remain solid, underpinned by improved gross margins and continued momentum in underlying sales volumes.

The slowdown is notable but not alarming in context. High-growth cycles in sports-related commercial activity - whether driven by broadcasting rights cycles, kit and merchandise demand, or digital platform subscriptions - rarely sustain their peak velocity across consecutive quarters. For reference, similar patterns of post-peak moderation have been observed across major sporting markets in Africa and South America, where clubs and leagues have rapidly expanded their commercial footprints in recent years. The broader African football landscape has seen significant commercial and squad-building activity of late; for instance, a recent orlando pirates update illustrates just how actively clubs in that market are investing and restructuring, reflecting genuine growth ambitions that depend on sustained commercial conditions.

What the Numbers Actually Tell Us

A 17 per cent revenue increase is, by most standards, a healthy expansion - it simply looks modest set against the exceptional growth of the previous two quarters. The Q4 2025 figure of 46 per cent was almost certainly amplified by cyclical factors: a major tournament window, a concentrated run of marquee fixtures, or the closing of significant rights or sponsorship deals. Q1 2026's 26 per cent suggested some natural cooling was already underway. The Q2 result confirms that trajectory, without indicating structural deterioration.

The more telling signal here is the margin story. If gross margins are improving even as headline growth moderates, that points toward better cost discipline, more efficient operations, or a more favourable product mix - potentially a shift toward higher-margin digital and streaming revenue streams rather than lower-margin physical goods or event-day income. In sports media and commercial rights environments, that transition has been a defining trend globally, with Indian, Brazilian and African markets increasingly central to where those digital audiences are being monetised.

Growth Expectations and What Comes Next

Looking ahead, the expectation of solid earnings growth despite the revenue deceleration will be the key metric for stakeholders to watch. Earnings growth that outpaces revenue growth is a sign of operational leverage - and in a sports commercial context, that often signals that the business of sport in a given market or segment has matured past its initial land-grab phase and is beginning to generate returns more efficiently.

That does not mean the ambition has dimmed. The markets most relevant to sports commercial expansion - Brazil's vast football-obsessed consumer base, India's cricket and football crossover audience, and Africa's rapidly urbanising and digitally connected fan population - continue to represent significant untapped upside. The Q2 figures reflect a pause in the growth curve, not a reversal. How the next two quarters perform, particularly against the backdrop of major competitions and transfer windows that typically drive commercial spikes, will determine whether 2026 closes as a year of genuine acceleration or one of managed consolidation.